By Segun Adaju and Ebipere Clark

It is common knowledge that one of Nigeria’s biggest infrastructural challenges is access to electricity with about 105 million of the country’s population on a grid that generates just 5,000MW. This amount is not enough to meet the current demand of those connected; forcing millions of electricity consumers and most particularly the 75 million off-grid population into using polluting fossil-fuel generators for lighting or be confined to darkness.

Over the past few years, there has been an increase in the awareness of and investments into off-grid renewable energy solutions such as pico-solar devices (e.g. solar lanterns and solar lighting solutions), solar home systems and mini-grids as a way to increase energy access in Nigeria. The advantages that these solutions have over the conventional grid include being cheaper and faster to deploy, as well as being more sustainable.

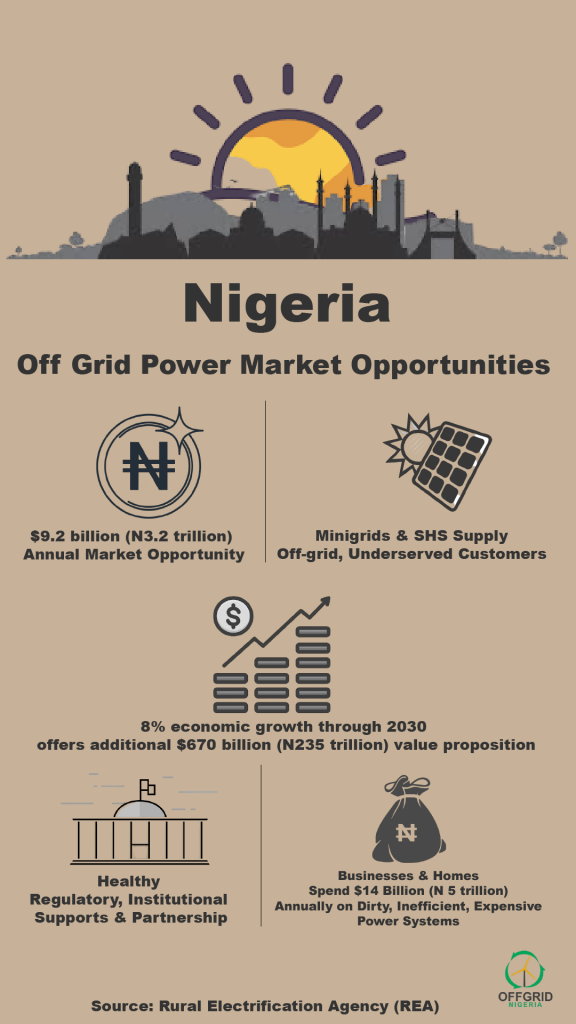

It is in recognition of the potentials for this market – estimated to yield $10billion annually in revenue with a savings of $6billion for Nigerians homes and businesses and reputed to be the world’s second largest off-grid market; that the Federal Government of Nigeria has put in place various policies and regulations to attract private sector investment.

The work around enabling environment has led to a corresponding increase in investor interest in Nigeria for the Off-Grid market and has led to several business models such as pay-as-you-go (PAYG) models with consumers; paying for the service via USSD bank transfer, scratch cards or collaboration with the agent banking networks of financial institutions. Many of these models are addressing consumer barriers around accessibility and affordability, and enabling quicker adoption of these off-grid systems and services.

However, the adoption of decentralized renewable energy technologies is still lagging in numbers and this is mainly due to the number of unbanked population who also make up majority of those without energy access. For instance, the Central Bank of Nigeria, estimates that there are approximately 33 million unique Bank Verification Numbers (BVN) in Nigeria, of which 25% are in Lagos and 80% in the southern states. This means that only 20% of those that use banks are in the North, the region which also has the larger concentration of those living off the grid.

Although there are mobile money products offered by banks and non-banking institutions, their market adoption penetration remains quite low with only 3% of transactions occurring through such channels. The reasons for this are numerous including a fragmented digital finance ecosystem with numerous operators promoting proprietary branded digital finance systems; restrictions on telecoms networks to deploy mobile money solutions; network complexity; a lack of interoperability (mobile money operator to mobile money operator); and poorly developed agent networks.

There is also a need for a clearer legal and regulatory framework in which mobile money (e-money) is differentiated from mobile banking, while market participants are not being equally treated, and the existence of mandatory requirements such as the Bank Verification Number (BVN). Low economic activity amongst the under-banked and unbanked, lack of awareness, products-needs gap, product complexity, high costs and usage difficulty are basic issues requiring measured intervention before telecom-led mobile money schemes are likely to have any real impact.

This means that achieving increased use of mobile money payments is not just about licensing telecom operators to offer mobile money product but also an improvement in infrastructure such as telecommunications and an expanded agent network.

The case could be made for better digital finance systems in order to scale PAYG solar solutions, but it is also important to see the entire structure around mobile payment systems as part of the larger goal of deepening financial inclusion in Nigeria. This is the goal of the Central Bank of Nigeria through its National Initiative on Finance Inclusion under the Development Finance Department. The initiative has a Financial Inclusion Secretariat which is made up of numerous stakeholders including banks, licensed Mobile Money Operators, the Nigerian Communications Commission, the Nigerian Postal Service and the insurance sector.

It is imperative for the power sector to be represented in this secretariat in order to contribute to shaping the digital finance ecosystem with regards to driving PAYG. It is even more urgent to have the Off-Grid operators – who are driving many of the Federal Government targets around rural electrification to also be a part of shaping the goals and outcomes of this

The Financial Inclusion Secretariat has set a target of adding 40 million low-income and unserved Nigerians into the banking system; as well as increasing financial access points from the current 70,000 to 500,000 by 2020. The secretariat is further working to deepen access to mobile and digital financial products and services, such as savings accounts, micro loans, insurance and pensions. This will also require raising about 500,000 agents by the three MMOs and six Super Agents spread across the country in order to capture new identities under the BVN scheme; as well as offer them products and services.

The challenge of a fragmented ecosystem is not limited to just digital finance but also to the three most important social infrastructure networks: energy (electricity), information (telecommunications) and finance (banking) and Identity and Biometrics. Each of these sectors is unable to expand in rural and peri-urban areas because of the absence of the other; yet the interconnection and interdependency of all four infrastructures are required for the digital finance network and reach to scale

The telecom sector is challenged with providing rural data services given the high cost of operating and maintaining diesel generators, along with the costs of providing security in areas of minimal economic activity. Whist the power sector complains about the costs and challenges of providing rural services due to the absence of rural banking platforms/digital finance and the difficulty with obtaining reliable data communications access. The banking sector also complains about the cost of providing agents in areas with insufficient levels of electricity, communications, and economic activities while Know Your Customer (KYC) requirements also present a cost to adding more people into the banking system.

With each sector currently working in silos and focusing solely on addressing its own issues, opportunities for synergies are missed. A telecom mast offering rural broadband services could and should be an anchor client of a mini-grid or micro power solution; a SANEF/NIPOST booth offering financial and postal services could be an anchor client for data and power; and PAYG solar consumers could interact with SANEF agents either with cash, or cashless opportunities through booth terminals or individual phones. Also, identity/ biometric platforms can be harnessed to meet KYC requirements easily since mobile phone users are required to register their phone lines biometrically.

Such collaborations and synergy will enable the expansion of PAYG solar products and services into rural areas where only 41% of the population enjoys energy access.

The hurdles for PAYG to scale in urban areas are less but nonetheless existent: how to enable financing for potential consumers and how to collect payments at scale.

PAYG providers will need to consider adapting their business models and collaborating with banks to achieve this. Banks can provide a range of services along the product value chain, from providing foreign currency exchange and letters of credit for the foreign-currency purchase of the PAYG asset to using banking agents to get collections from customers who have leased products from the bank’s leasing subsidiary.

Without the improvement of the reliability of the four social infrastructure networks in rural areas, there is unlikely to be significant increases in the deployment of PAYG products and services.

It is encouraging that the CBN has recently released regulations for payment service banks which allow promoters such as banking agents, telcos, retail chains and MMOs to set up banks that will leverage on technology and agents to increase financial inclusion in Nigeria.

There will continue to be a need for systemic collaboration between the finance, telecommunications, power and identity and biometric ecosystems until it gets to the point of resilience and reliability where each of the services can simply and seamlessly plug into the other’s network to achieve the scale in their operations.

We are confident that the initiatives started by the Financial Inclusion Secretariat together with the effect of market forces, will bring about the improvements that PAYG solar companies can leverage on to grow.

Mr. Segun Adaju – Is President Renewable Energy Association of Nigeria (REAN) and CEO of Consistent Energy

Mr. Ebipere Clark – Is a Senior Advisor on Energy in the Officer of the Central Bank Governor